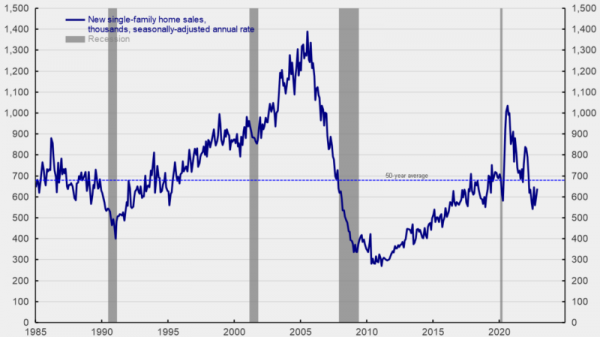

Sales of new single-family homes rose again in November, increasing 5.8 percent to 640,000 at a seasonally-adjusted annual rate from a 605,000 pace in October. The November gain was the third increase in the last four months, but sales are still down 15.3 percent from a year ago and down 38.2 percent from the August 2020 post-recession peak. November sales remain below the 50-year average selling rate (see first chart).

Sales of new single-family homes were up in two of the four regions in November, rising 21.3 percent in the Midwest, while sales in the West increased 27.6 percent. Sales in the Northeast, the smallest region by volume, fell 8.5 percent, and sales in the South, the largest by volume, decreased 2.1 percent.

Over the last 12 months, sales were down in two of the four regions, led by a 26.6 percent fall in the West and a 15.0 percent decline in the South. There is a 3.6 percent gain in the Midwest while the Northeast region shows a rise of 26.5 percent from November 2021.

The median sales price of a new single-family home was $471,200 (see second chart), down from $484,700 in October (not seasonally adjusted), putting the 12-month average price at a record high of $448,000 (see second chart). Meanwhile, 30-year fixed-rate mortgages were 6.27 percent in late December, down from 7.08 percent in mid-November but up sharply from a low of 2.65 percent in January 2021. The combination of high prices and elevated mortgage rates reduces affordability and squeezes buyers out of the market.

The total inventory of new single-family homes for sale fell 1.7 percent to 461,000 in November. That puts the months’ supply (inventory times 12 divided by the annual selling rate) at 8.6, down 7.5 percent from October but 38.7 percent above the year-ago level. Inventory and the months’ supply remain very high by historical comparison (see third chart). The high level of prices, elevated inventory, and elevated mortgage rates should continue to weigh on housing activity in the coming months and quarters. The median time on the market for a new home remained rose in November, coming in at 1.9 months versus 1.5 in October but remains very low in historical context.

Meanwhile, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in December, coming in at 31 versus 33 in November. That is the twelfth consecutive drop and the fifth consecutive month below the neutral 50 threshold. The index is down sharply from recent highs of 84 in December 2021 and 90 in November 2020 (see fourth chart).

Components of the Housing Market Index were mixed in December. The expected single-family sales index rose to 35 from 31 in the prior month, the current single-family sales index was down to 36 from 39 in November, and the traffic of prospective buyers index was unchanged for the month (see fourth chart).